In 2023, the financial world was rocked by a series of bank failures. Silicon Valley Bank was the first domino to fall; Signature Bank and First Republic Bank followed suit.

The collapses sparked widespread concerns about the stability of the larger US banking system and what risk factors could threaten to topple other, larger banks.

CBS Professor Tomasz Piskorski wasn’t content to speculate. So, along with several colleagues, he sought to assess how specific economic pressures impact bank stability in the United States.

He specifically wanted to investigate the impact of rising interest rates. The US banking sector, he explains, is usually highly leveraged. “A typical bank in the United States is 90 percent debt-financed and only about 10 percent equity,” says Piskorski. “Most of the debt funding comes in the form of deposits, about half of which are insured … so if you have $100 million worth of assets financed with $90 million of debt, in principle, even a 10 percent decline in the value of your assets due to high interest rates could result in insolvency.”

The other critical backdrop for this research was the distress of the commercial real estate (CRE) sector, which has struggled since pandemic-related office closures and the rise of remote and hybrid work. “For an average regional bank in the United States, about 25 to 30 percent of their assets are CRE loans, which finance office buildings, apartments, industrial warehouses, hotels, and more,” Piskorski says. These properties typically have long-term leases, which can make their cash flows particularly vulnerable to higher interest rates.

The resulting study analyzes the interplay between monetary policy changes and the vulnerabilities of banks with high exposure to CRE loans and provides insights about potential measures that could mitigate the risk of other dominos falling in the future.

Key Takeaways:

- The findings suggest the current primary pressure on banks stems from high interest rates, with CRE distress exacerbating the problem.

- Recent increases in interest rates have led to an aggregate loss of up to $2 trillion in the value of US bank assets.

- Approximately 14 percent of all CRE loans and 44 percent of office loans are in negative equity, where property values are less than outstanding loan balances. One-third of all CRE loans and the majority of office loans face substantial refinancing challenges due to elevated interest rates.

- The combined impact of asset value declines and CRE loan defaults could significantly increase insolvency risks for a substantial number of US banks, particularly smaller regional banks.

How the research was done: To measure the impact of the dual economic pressures of high interest rates and CRE distress, the researchers examined the asset composition of 4,844 FDIC-insured banks in the United States — including how they finance themselves in terms of deposits and the percentage of uninsured deposits they hold. They then quantified the decline in the value of bank assets based on current interest rate hikes.

The researchers also employed a detailed loan-level analysis of CRE loans, using data from the commercial mortgage-backed securities market to estimate current loan-to-value ratios and debt service coverage ratios.

What the researcher found: The analysis painted a bleak picture of the current reality for the US banking sector. “US banks have lost about $2 trillion in aggregate in the value of their assets since the beginning of the Federal Reserve’s tightening cycle,” says Piskorski. This decline has eroded many banks’ capital buffers, making them more vulnerable to adverse credit events.

The research also highlights that about 14 percent of all CRE loans and 44 percent of office loans are currently in negative equity. Furthermore, around one-third of all loans, including a majority of office loans, are likely to face severe refinancing challenges due to the more than doubling of debt costs following the interest rate hikes.

These factors collectively increase the risk of bank defaults, potentially reaching levels comparable to or surpassing those seen during the Great Recession. However, these findings don’t necessarily translate into a worst-case scenario. “The behavior of depositors is an important factor,” explains Piskorski. “As long as depositors are keeping money in these banks at below-market interest rates, they essentially subsidize the banks.” Regulators have come to the rescue, too, by establishing safeguards like the Bank Term Funding Program.

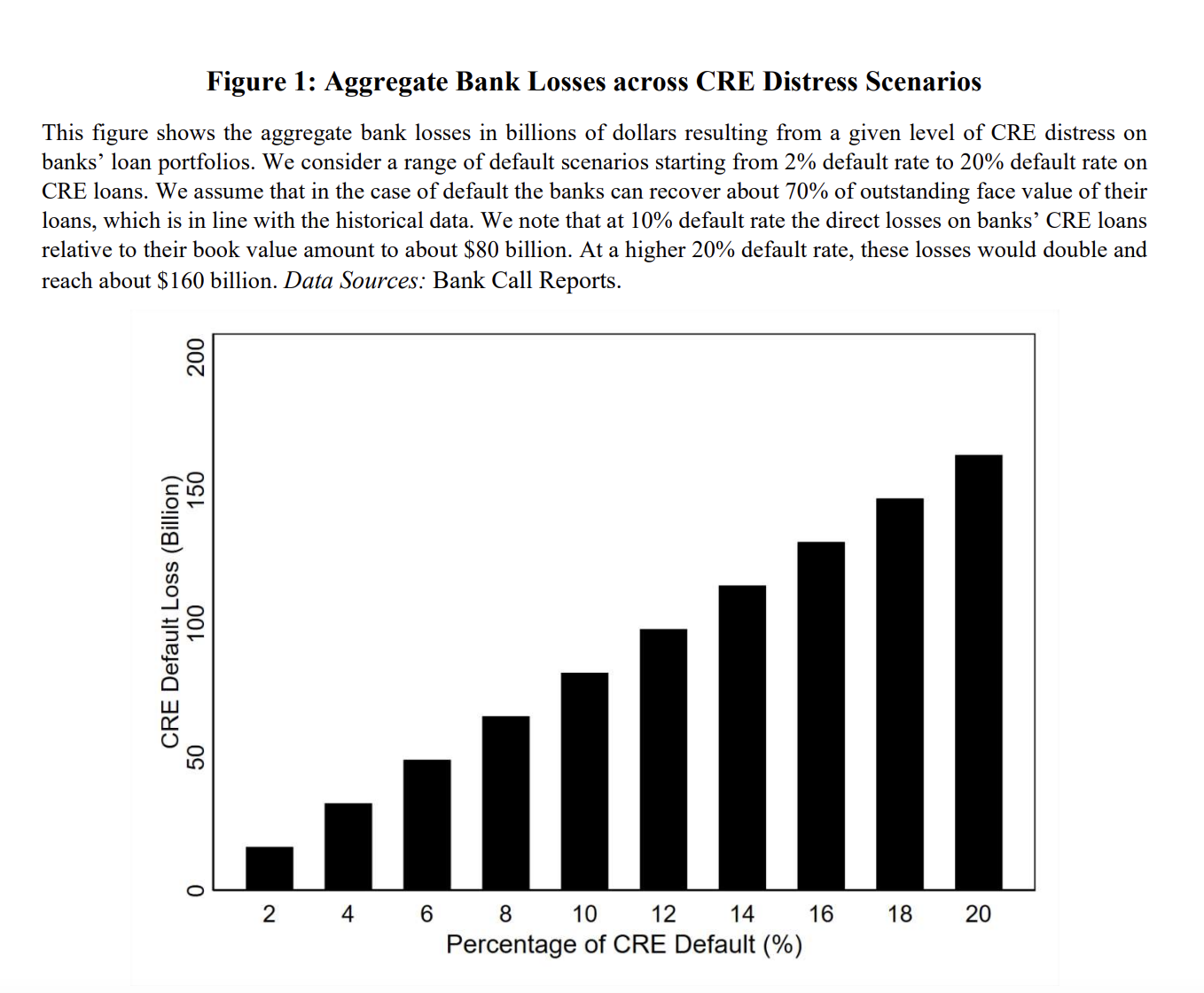

Another finding was that direct losses to banks due to CRE distress alone are not as overwhelming as feared. At a 10 to 20 percent default rate, these losses amount to about $80 billion to $160 billion. If CRE distress had occurred in early 2022 when interest rates were still low, the banking system could have absorbed the losses without a single failure. Even in the worst-case scenario, the potential losses from CRE distress would have amounted to less than 10 percent of the total equity in the banking system, providing a sufficient cushion.

Why the research matters: The study underscores the tenuousness of the US banking system in the current high interest rate environment. Significant losses in asset values, coupled with distress in the CRE sector, pose a substantial risk to banks — particularly smaller regional banks with high exposure to CRE loans and uninsured deposits.

“Elevated interest rates expose banks to the risk of runs by depositors, especially uninsured ones. Commercial real estate distress adds to that risk. The combination of these two factors means we’re in a system that’s quite fragile right now," says Piskorski.

Regulatory interventions, such as creating credit facilities and providing guarantees for depositors, have helped short-circuit potential bank runs in the past. But Piskorski believes these are a Band-Aid solution to a larger, more entrenched problem. He argues that there’s an urgent need for additional policy changes to mitigate ongoing risks. In the longer term, he advocates for stricter capital requirements to align banks’ capital ratios closer to those of less-regulated non-bank lenders, which retain more than twice as much capital buffers as banks do.

Such measures could make the US banking system more resilient and better equipped to handle future adverse shocks — and help ensure one downed domino doesn’t lead to a cascade.

Adapted from “Monetary Tightening, Commercial Real Estate Distress, and US Bank Fragility,” by Tomasz Piskorski from Columbia Business School, Erica Xuewei Jiang from the USC Marshall School of Business, Gregor Matvos from the Kellogg School of Management at Northwestern University, and Amit Seru from the Stanford Graduate School of Business.